Can the European Manufacturing Industry Capitalize on the Humanoid Momentum?

Structural change in the manufacturing industry, especially in the automotive sector, is accelerating the search for new growth opportunities. Humanoid robotics is gaining strategic relevance as a future market that closely aligns with established competencies in automation, mechatronics, and industrial manufacturing. Early engagement in the humanoid hardware value chain offers European manufacturers a tangible opportunity to capture value in this emerging field. Market projections indicate substantial growth potential. The global humanoid robotics market is expected to reach a volume of approximately USD 30 billion by 20301. Long-term scenarios project a worldwide installed base of several hundred million humanoid robots by 20502. These developments highlight the relevance of early engagement with the underlying value chain.

This whitepaper analyzes the role of hardware in the context of the industrialization of humanoid robots. Despite advances in artificial intelligence, the economic viability, reliability, and scalability of humanoid systems are largely determined by hardware components. At present, standardized hardware architectures are lacking, and key components such as actuators, gearboxes, batteries, and sensors only partially meet industrial requirements in terms of robustness, lifetime, and cost structure.

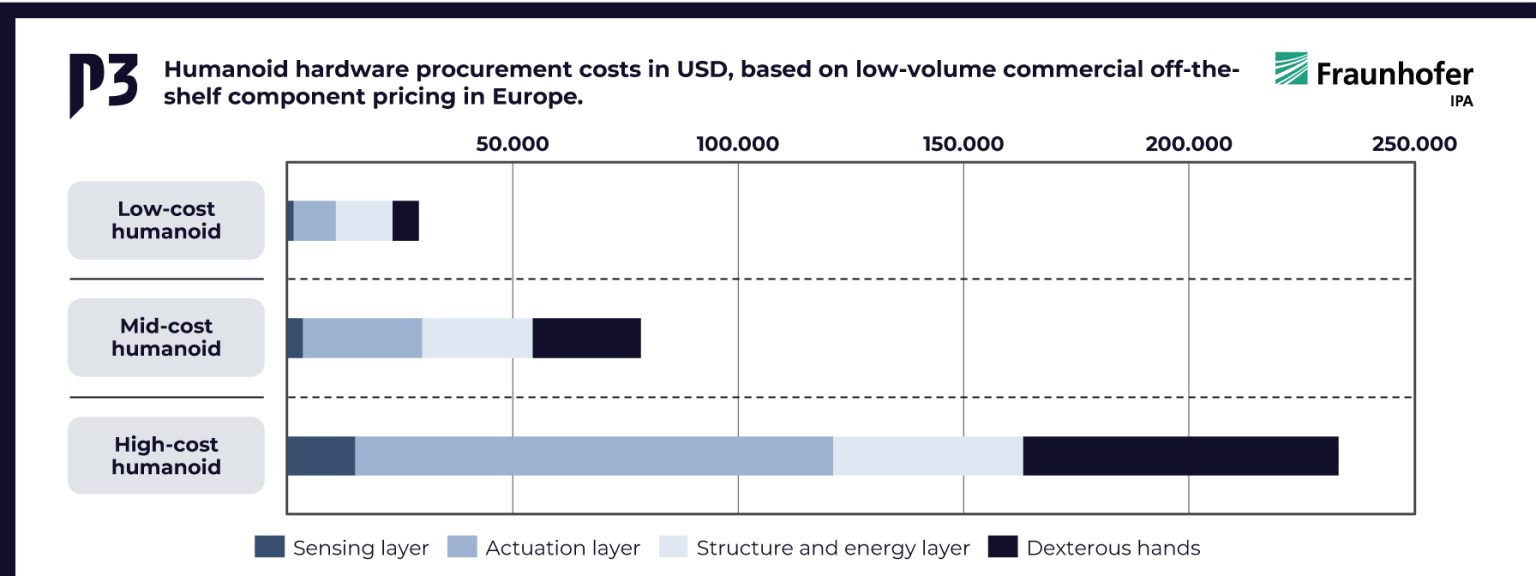

To quantify these challenges, the study combines a layered analysis of humanoid hardware architectures with a bottom-up cost model. The resulting cost scenarios, summarized in Figure 1, enable a structured comparison of low-, mid-, and high-cost humanoid configurations and illustrate how different hardware choices translate into overall system cost. The analysis highlights hardware components that dominate overall expenditure and represent key challenges for cost-efficient scaling, particularly for humanoid systems intended for continuous industrial operation.

For European manufacturers, this represents a concrete strategic opportunity. The capabilities required for humanoid hardware, including precision mechatronics, advanced manufacturing, and system integration, align closely with established strengths of European automotive suppliers and mechanical engineering companies. Capturing value in this emerging market will depend on a focused engagement in the development and industrialization of cost- and performance-relevant hardware components, combined with early and close collaboration with humanoid OEMs.

Download the complete whitepaper with all insights here for free: